Top 10 Asia’s Richest 2021

Asia’s top 10 richest people, as of June 12, 2021

Mukesh Ambani: $84.3 billion

Gautam Adani: $77.0 billion

Zhong Shanshan: $71.2 billion

Ma Huateng: $60.1 billion

Jack Ma: $48.9 billion

Zhang Yiming: $44.5 billion

Colin Huang: $43.4 billion

Zeng Yuqun: $39.1 billion

Tadashi Yanai: $38.9 billion

William Ding: $35.7 billion

Mukesh Ambani: $84.3 billion

Ambani’s fortune has risen to almost $84 billion, according to the Bloomberg Billionaires Index, making him the world’s 12th richest person. So far in 2021, Ambani has invested $7.62 billion. Mukesh Ambani of the Reliance Group is Asia’s richest man, with $84.3 billion.

Reliance was formed in 1966 as a modest textile firm by his late father, Dhirubhai Ambani, a yarn trader.

With the debut of its 4G phone service Jio in 2016, Reliance started a pricing war in India’s hyper-competitive telecom sector.

During the Covid-19 siege, Ambani raised more than $20 billion by selling a third of Jio to a group of investors that included Facebook and Google.

Gautam Adani: $77.0 billion

Adani is second with a $77 billion wealth. Adani’s fortune, on the other hand, has risen to $77 billion, with a $43.2 billion increase so far in 2021. According to Bloomberg figures, Adani is the 14th richest person on the planet. Gautam Adani, an infrastructure mogul, owns India’s largest port, Mundra, in his home state of Gujarat. Adani owns Abbot Point, a contentious Australian coal mining project whose Carmichael coal mine is touted as one of the world’s largest.

In September 2020, Adani purchased a 74% share in Mumbai International Airport, India’s second busiest.

Zhong Shanshan: $71.2 billion

Zhong Shanshan is a rich Chinese businessman. Nongfu Spring, a bottled water company that went public in Hong Kong in September 2020, is chaired by Zhong Shanshan.

He is the founder and chairman of Nongfu Spring and the primary shareholder of Beijing Wantai Biological Pharmacy Enterprise.

Ma Huateng: $60.1 billion

Ma Huateng (also known as Pony Ma) is the chairman of Chinese internet behemoth Tencent Holdings, which is one of the country’s most valuable companies by market capitalization. He is the founder, chairman, and CEO of Tencent, Asia’s most valuable corporation, one of the world’s largest Internet and technology corporations, as well as one of the world’s largest investment, gaming, and entertainment conglomerates. In December 2018, the company’s music-streaming business, Tencent Music, went public on the New York Stock Exchange.

Jack Ma: $48.9 billion

Jack Ma Yun is a Chinese business entrepreneur, philanthropist, and investor. Alibaba Group, a multinational technological conglomerate, is his co-founder and former executive chairman. He also co-founded the private equity business Yunfeng Capital. Ma is a staunch supporter of a market-driven, open economy. In September 2019, Alibaba’s executive chairman, Jack Ma, stepped down and was replaced by CEO Yong Zhang, also known as Daniel Zhang.

Zhang Yiming: $44.5 billion

One of China’s largest media content platforms, Beijing ByteDance, is chaired by Zhang Yiming. President Trump ordered ByteDance to sell TikTok’s U.S. businesses in August 2020; a potential deal with Walmart and Oracle is still in the works. Zhang’s personal wealth is estimated to be $44.5 billion, according to the Bloomberg Billionaires Index. Zhang Yiming stated on May 20, 2021 that he would be stepping down as CEO of ByteDance at the end of the year and shifting to a new position within the company.

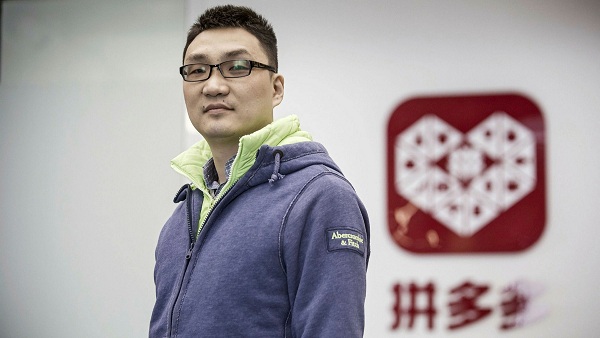

Colin Huang: $43.4 billion

Colin Huang, also known as Huang Zheng, is the chairman of Pinduoduo, one of China’s largest e-commerce platforms. Huang, a serial entrepreneur, previously launched Xinyoudi, an online game company, and Ouku.com, an online e-commerce platform. Pinduoduo raised $1.6 billion in a July 2018 IPO in the United States, despite backlash over its alleged sale of counterfeit goods.

Zeng Yuqun: $39.1 billion

Contemporary Amperex Technology (CATL), one of the world’s major providers of batteries for electric vehicles, was founded and is led by Zeng.

BMW, Volkswagen, and Geely are among the clients of CATL, which went public on the Shenzhen Stock Exchange in 2017.

Tadashi Yanai: $38.9 billion

Tadashi Yanai founded and controls Fast Retailing, the parent company of the Uniqlo apparel chain, which is listed on the Tokyo Stock Exchange.

Theory, Helmut Lang, J Brand, and GU are among Fast Retailing’s other brands.

On revenue of $19 billion, the corporation declared a net profit of $853 million for the fiscal year ending August 2020.

William Ding: $35.7 billion

Netease, one of the world’s leading online and mobile games companies, is led by William Ding.

Mojang, a Microsoft company, and Blizzard Entertainment are among Netease’s business partners.

Faced with stiff competition from Chinese rival Tencent in the games market, Netease expanded into movies, online music, and e-commerce.

10 Richest People in the World

| Names of Richest People |

Fortune |

| Bernard Arnault & Family |

$186.3 billion |

| Jeff Bezos |

$186 billion |

| Elon Musk |

$147.3 billion |

| Bill Gates |

$125.5 billion |

| Mark Zuckerberg |

$114.7 billion |

| Warren Buffet |

$108.7 billion |

| Larry Ellison |

$102.3 billion |

| Larry Page |

$100.2 billion |

| Sergey Brin |

$97.1 billion |

| Amancio Ortega |

$89 billion |

…

Worlds Richest

With a net worth of $194 billion, Amazon founder Jeff Bezos is the wealthiest person on the planet. Following him is LVMH Chief Executive Bernard Arnault, who has a fortune of S173 billion. Elon Musk, the CEO of Tesla, ranks third on the list, with a fortune of over $169 billion.

Jeff Bezos

In 1994, Jeff Bezos launched e-commerce behemoth Amazon from his Seattle garage. In July 2021, he will step down as CEO and become executive chairman.

")