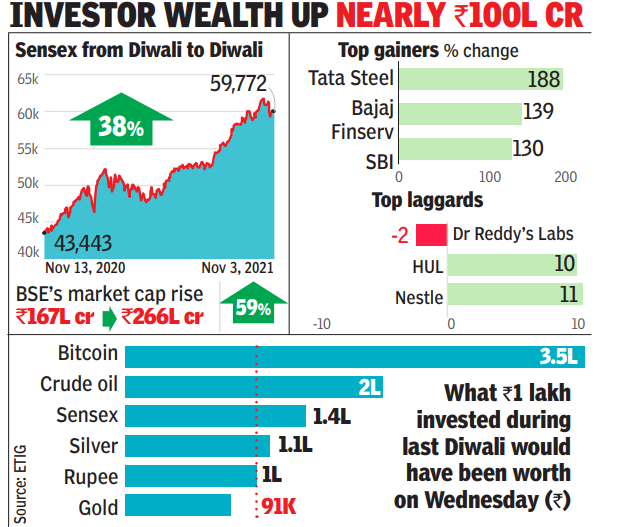

MUMBAI: Investors on Dalal Street were richer by about Rs 99 lakh crore during Samvat year 2077 that ended on Tuesday, riding on strong across-the-board buying that also led to a 38% jump in the sensex to its current close at 59,772 points. The rise was the best in the last 12 years while the gain in investors’ wealth—in terms of BSE’s market capitalisation—was the best ever, official data showed.

The year ended with BSE’s market cap at Rs 266 lakh crore ($3.6tn), which elevated India to the sixth largest market spot in the world in terms of market value. Samvat 2077—the calendar followed by mainly the trading community on Dalal Street—will go down as one of the best years in terms of returns and the regularity with which the leading indices hit new all-time highs, even though the economy struggled due to the ongoing Covid-induced pandemic, market players said.

Metals, banking & financial services, and software exporters led the rally while pharma and FMCG stocks witnessed muted gains in prices. The gains came on the back of nearly Rs 1.25 lakh crore worth of net buying of stocks by foreign institutional investors, while domestic institutions, which include mutual funds, insurance companies, banks and others financial companies, were net sellers at about Rs 34,700 crore, CDSL and BSE data showed.

The year will also be marked as the year when new age consumer-facing tech-enabled companies, for years being privately held by a handful of private equity-venture funds, started getting listed. The trend, often called private going public by merchant bankers and analysts, was led by food delivery company Zomato and soon followed by CarTrade. A host of such companies, that include FSN E-commerce (Nykaa), PB Fintech (Policybazaar) and One 97 Communications (PayTM), are now in various stages of going public during Samvat 2078.

According to Yesha Shah, head of equity research, Samco Securities, Samvat 2077 could be termed as the year of unicorns and technology companies. Technology adoption, which was formerly limited to certain sectors, has now become mainstream, Shah wrote in a note to clients.

“With the advent of e-commerce, (the) move to online prompted major alterations in sectors such as travel, hotels, restaurants, entertainment, and education. With increased internet access, smartphone penetration, and 5G modernization in India, the user base of Indian tech-driven fintech, edtech, healthtech and e-commerce start-ups is rapidly growing. This trend is backed up by India’s growing list of Unicorns, which has resulted in the nation having the world’s third largest start-up ecosystem. As a consequence, it was not unexpected that 2021 provided an appropriate opportunity for numerous such start-ups to make their public market debuts,” Shah wrote.

The year’s rally on D Street also catapulted some Indians to the club of the richest people in the world and Asia. The list includes Mukesh Ambani of Reliance Industries, Gautam Adani of Adani Group and Radhakishan Damani of D-Mart.

NEW DELHI: A day after the government announced a mega bailout package for the telecom industry, Bharti Airtel chief Sunil Mittal said the company will opt for the four-year moratorium on spectrum and AGR payments, which will help it conserve a cash outgo of Rs 35,000-40,000 crore that would be used for network and other capital expansion programmes.

“Overall cash flows of the government has to be invested back in the country and industry. It has to be utilised. There will be no dividend from this,” said Mittal.

Mittal also pitched greater collaboration between various telecom companies on the front of infrastructure — such as fibre, spectrum and towers — so that a strong network can be built for consumers.

He said he will talk to rivals such as Mukesh Ambani of Reliance Jio, after having initiated dialogue with Vodafone global CEO Nick Read and his Indian partner and industrialist Kumar Mangalam Birla.

“Ambani in his statement yesterday said that it’s time for the industry to come together… and build connectivity network for the digital vision of India. Responding to that statement, I would say, yes, time has come for all of us, the three plus one government operator, to close ranks, and to start to work together, work as Team India, for the telecommunications and digital dream, rather than being fierce competitors. All this while we will compete in the marketplace.”

MUMBAI: Banks led by State Bank of India (SBI) have called on the Indian government to give debt-laden Vodafone Idea more time to clear its tax dues and spectrum fees, two bankers and a government official familiar with the matter said.

An Indian court last year ordered the mobile carrier, a joint venture between the Indian unit of Britain’s Vodafone Group and Aditya Birla Group’s Idea Cellular, to pay just over $8 billion to the government to settle long-standing dues. Vodafone has a stake of about 44% in the company and Aditya Birla owns nearly 27%.

In June, Vodafone Idea’s then non-executive chairman Kumar Mangalam Birla warned that without a government reprieve the Indian mobile carrier’s “financial situation will drive its operations to an irretrievable point of collapse”.

Vodafone Idea’s gross debt as of June 30 was 1.9 trillion rupees, comprising of deferred spectrum payment obligations of 1.06 trillion rupees and an adjusted gross revenue liability of 621.8 billion rupees, its latest stock exchange filing in June showed.

The adjusted gross revenue is the usage and licensing fee that telecom operators are charged by the Indian government.

The mobile operator also reported that it owes 234 billion Indian rupees ($3.18 billion) to financial institutions.

Senior SBI officials and representatives of the Indian Banks’ Association (IBA) met finance and telecom department officials this month and proposed an immediate breather on the repayment of spectrum dues, the two bankers and the government official, who requested anonymity, told Reuters.

“We’ve had these discussions with the banks but the issue is the finance ministry needs to be comfortable with the measures,” the government official said.

SBI, IBA, and the finance and telecom departments did not respond to Reuters requests seeking comment.

The government is also evaluating whether to take a small stake in financially struggling Vodafone Idea, in order to allay investor concerns regarding the future of the telco.

The company is facing a repayment of 5-10 billion rupees of non-convertible debentures around January, one of the bankers said.

Vodafone Idea declined to comment. Vodafone Group did not immediately reply to an email seeking comment. An Aditya Birla Group spokesman declined to comment.

Vodafone Idea had cash and cash equivalents of 9.2 billion rupees at the end of June, a transcript of a company conference call published on its website said.

“All eyes are on New Delhi right now as banks are getting increasingly nervous,” another banker with exposure to Vodafone Idea said.

The bankers have also proposed providing some relief to Vodafone by restructuring its dues, one government official and two bankers said.

Birla stepped down as chairman early last month after appealing for the government bailout.

The government has been considering a broader package to help a telecom industry disrupted by the 2016 entry of Mukesh Ambani-controlled Reliance Jio, which shook up the market with its free voice and cut-price data plans.

A smartphone widely believed to be priced below $50, likely the world’s cheapest, will start selling a week from now. If Mukesh Ambani’s JioPhone Next, an Android device custom-built for India by Alphabet Inc.’s Google, is a hit in the price-conscious market, it will solve one problem for banks while posing another.

With the country’s remaining 300 million feature-phone users going online, there will be a surge of customer data that can stand in for collateral. The question is, how will banks get their hands on it?

An answer has come from iSPIRT, a small band of policy influencers quietly setting up technology standards for India’s digital markets, inducing firms to enter new, open-network markets from online payments to healthcare.

The Bangalore-based group is championing a fresh set of players — account aggregators — to unlock a much sought-after prize: Bringing into the folds of formal credit the 80% of adults in developing countries (40% in rich nations) who don’t borrow money from traditional institutions.

But these people and their micro enterprises are increasingly online thanks to innovations like JioPhone Next. They’re paying rents, rates and utility bills and receiving payments on their smartphones, scattering their footprints all over the internet. Account aggregators will gather those digital crumbs for people to share their own data in a machine-readable format for a bank loan application.

Introducing a layer of consent managers is important. Emerging-market borrowers can have many types of accounts-based relationships. Yet they can be useless to banks if they can’t present a composite picture of their financial lives to access formal loans that get monitored by credit bureaus. More than three-fifths of India’s adult population is either invisible to credit scorers or not considered worth the trouble by standard lending institutions.

In an advanced economy like the U.S., services such as Experian Boost and LenddoScore help narrow the subprime borrowers’ visibility gap by getting them to voluntarily submit their utility or video-streaming bills to demonstrate creditworthiness. But in an emerging market with low financial literacy, banks would rather leave the bottom of the pyramid to lenders who know the borrower in real life or have some social leverage on her — such as micro-finance firms that lend to groups of women.

Conversely, tech platforms, intimately aware of their customers’ online behavior, can match them with loans, collecting fees while leaving risks with the banks. Jack Ma’s Ant Group Co. cornered nearly a fifth of China’s short-term consumer debt before Beijing broke up the game.

Not every country can afford to bring out the heavy artillery against its private sector: Politics wouldn’t allow it. Aggregators can be a much softer tool for keeping the lending market fair, giving banks a reasonable economic chance to compete with data-rich tech giants.

Take JioPhone Next. It will spew out data about a large segment of sparsely banked population. Jio, Ambani’s 4G telecom network, will capture some of it as subscribers of its cheap data plans buy groceries from JioMart, an online partnership with neighborhood stores across India. Google will also get valuable data about users’ location and search queries. Facebook Inc. will exploit its own knowledge, as the social media giant adds to its half-a-billion-strong Indian customer base for WhatsApp and a growing craze for Instagram Reels, a video-sharing platform. Unsurprisingly then, Google wants to influence India’s deposit market, and Facebook is nibbling into the small business loans pie.

When it comes to real-time data, banks can never match the platforms’ clout. But account aggregators’ snapshots can help them catch a break.

Just enough additional data that will tell them if a customer is more creditworthy than suggested by a low (or no) credit score can make a big difference to profit, especially as banks won’t have to pay hefty fees to the likes of Jio, Google or Facebook for their proprietary assessments. By owning and explicitly sharing their data, customers will avoid getting trapped in the tech industry’s biased algorithms. Tiny enterprises will be able to show their cash flows to lenders by pooling everything from tax payments to customer receipts. Once telecom firms come on board, an affordable “buy-now-pay-later” plan on a refrigerator purchase will become possible for a low-income family that pays its phone bills regularly .

Aggregation, being a utility, will be like tap water to platforms’ Evian, and be priced accordingly. Who will own the pipes? Walmart Inc.’s PhonePe, which runs India’s most popular digital wallet, has received an in-principle approval to be an aggregator from the central bank. Eight banks, which between them account for 48% of all accounts in the country, have agreed to use the framework, which went live Thursday.

It’s a good start. Banks desperately need some help to stay in the money game. Or they’ll just go crying to regulators and ask them for special protections against Big Tech. That would hurt experimentation and delay the credit revolution that $50 phones can unleash.

The gap between the top three UPI apps and WhatsApp Pay is quite epic.

It took a good over a two-and-a-half-year period for Facebook-owned WhatsApp to roll out its much talked about payments service in November 2020 from around February 2018 when the messaging giant had started testing the feature. In October 2020, a month before the rollout, WhatsApp Payments or WhatsApp Pay had processed 70,000 UPI transactions amount to Rs 9.32 crore. In its first month (November) of approval from the National Payments Corporation of India, which operates the UPI payments infrastructure, the figures jumped to an impressive 3.1 lakh transactions worth Rs 13.87 crore. However, the growth, in transactions primarily, since its launch till February 2021 arguably hasn’t picked the kind of pace one would have expected from WhatsApp that counts over 500 million users in its biggest market India. As per NPCI data, WhatsApp managed to scale to 5.5 lakh UPI transactions worth Rs 32.41 crore in February.

“The reason is very clear. It is the lack of use cases. Right now, WhatsApp is offering peer-to-peer (P2P) payments. There is no geography where just on the back of P2P payments, digital payments have proliferated. They don’t have those P2M transactions or use cases defined really well,” Arnav Gupta, an analyst at Forrester Research told Financial Express Online.

WhatsApp didn’t reply to an email seeking comments for this story.

The Roadblock

While the company has been studying the digital payments market for at least three years, the business side of the platform has been a roadblock for the company as WhatsApp hasn’t been able to further evolve it and connect it back to payments proposition. For example, Gupta said that WhatsApp is only a unilateral channel of communication for enterprises to speak to their customers. For instance, a travel portal can send a customer’s travel tickets and invoice on WhatsApp but he/she cannot talk back to the company while there are very few and limited use cases where there are chatbots set-up. According to Gupta, that is the struggle WhatsApp is going through.

WhatsApp’s viral growth and the kicking off of its networking-effects in the early days was certainly the stuff of legend. However, that has not translated yet in its payments business that has been approached in fits and starts. “WhatsApp’s desire to keep its interface consistent across geographies meant it was unable to create a dedicated payments interface within the app for India despite the exploding UPI market. This means it lags in a market it could have clearly dominated. Even when we look at the data in the past three months, its transactions have fallen in January 2021 from a December 2020 high,” Utkarsh Sinha, Managing Director, Bexley Advisors, a boutique investment bank firm, told Financial Express Online.

Importantly, WhatsApp Pay rollout had coincided with the NPCI announcement in November that third-party applications offering UPI payments service can process a maximum of 30 per cent of the transaction volumes starting January 1, 2021. The decision, according to an NPCI statement, was taken to “address the risks and protect the UPI ecosystem as it further scales up.” Moreover, NPCI had allowed WhatsApp to launch payments service in a graded manner to a maximum of 20 million registered users in UPI.

“Limiting the number of digital payments that could be made via payment apps adversely affected all other wallets, including WhatsApp,” Prabir Chetia, Head – Business Research & Advisory, Aranca told Financial Express Online. Moreover, the entire payment section had a step-by-step launch with no marketing push. “There was no big bang marketing campaign to announce its entry into the payment space. Hence, the awareness regarding this new offering of WhatsApp is very low. Consumers who are tech-savvy and active users of the app may know about it and even use it, but many others still view it as a communication tool,” added Chetia.

Missing the Bus

The thought perhaps at WhatsApp back in 2017 was about leveraging the customer loyalty for its messaging environment to plug-in the payments service. This would have meant for customers to remain within WhatsApp instead of exiting it and using Paytm, PhonePe, Google Pay, others for transacting online. However, a nearly three-year long period from testing the service to its eventual launch has perhaps impacted its growth. “Had they been able to launch then (in 2018), they would have evolved like others. They have missed the bus by over two years. Having said that, their partnership with Jio could be a potentially viable business model and can create some buzz. But JioMart is not available on WhatsApp in all the cities currently,” said Gupta.

In April 2020, Facebook had picked up a 9.99 per cent stake in Jio Platforms at $5.7 billion. The deal had supporting India’s vast small business base digitally as its key focus. Moreover, Mark Zuckerberg at a company event in December 2020 with Mukesh Ambani had revealed that WhatsApp has 15 million business app users from India. “Jio brings digital connectivity, WhatsApp now with WhatsApp Pay brings digital interactivity, and the ability to move to close transactions and create value, and Jio Mart brings the unmatched online and offline retail opportunity, that gives our small shops which exist in villages and small towns in India, a chance to digitise and be at par with anybody else in the world,” Ambani on his part had said. Jio and WhatsApp have more than 400 million customer base in India.

“WhatsApp has been ironing out its strategy for the space since 2017. But that has led it to concede valuable space to the current incumbents. If WhatsApp was aggressive in payments to start with, a lot of the current competition would have struggled to gain a foothold,” said Sinha.

The Epic Gap

Current UPI payments incumbent PhonePe had cornered an impressive 42.5 per cent share of the 2,292.90 million UPI transactions in February, as per NPCI data. Walmart’s payment arm in India – PhonePe had processed 975.53 million UPI transactions amounting to Rs 1.89 lakh crore. Likewise, Google Pay, which lost the top spot to PhonePe in December 2020, was the second-largest UPI app in February processing 827.86 million transactions (36 per cent of total UPI volume) worth Rs 1.74 lakh crore. On the other hand, Paytm was still the distant third player in February recording 340.71 million transactions involving Rs 38,493.52 crore. It had processed 332.69 million transactions worth Rs 37,845.76 crore in the preceding month.

The gap between the top three UPI apps and WhatsApp Pay is quite epic. “WhatsApp has a huge user base. However, these users are using it as a communication tool. Will they become loyal to its payment solution? I think it is unlikely,” said Chetia. Despite a large user base, those living in Tier-III cities and beyond are less likely to use WhatsApp for payments. That’s also because, unlike its large competitors, WhatsApp doesn’t offer cashback and other add-on services as incentives. “Even if they build out certain use cases, still daily active users on other platforms are far too much. So, I don’t think WhatsApp would be in a leadership position,” said Gupta. However, it might be too early to call any winners in the UPI space. WhatsApp still owns the Bharat behind India, and their entry is a significant tectonic shift that might unlock a lot of disruptive value in the long term. It is precisely because of their scale that this value potential exists.