RBI needs to ensure nascent revival of economic activity shows signs of durability: Governor Shaktikanta Das

[ad_1]

Read More/Less

Reserve Bank of India Governor Shaktikanta Das said the central bank needs to ensure that the nascent revival of economic activity shows signs of durability and sustainability. At the Monetary Policy Committee (MPC) meeting, held between October 6 and 8, 2021, Das referred to an ever evolving and dynamic environment, with the outlook overcast by several uncertainties including the fact that the pandemic is far from over.

“At this critical juncture, our actions have to be gradual, calibrated, well-timed and well-telegraphed to avoid any undue surprises,” the Governor said.

Professor Varma’s take

According to the Minutes of the MPC meeting released by the RBI on Friday, Jayanth R Varma (Professor, Indian Institute of Management, Ahmedabad) was the only MPC member who voted against the accommodative stance and was not in favour of the decision to keep the reverse repo rate at 3.35 per cent. He had taken a similar stand at the previous MPC meeting.

Varma reiterated that the Covid-19 pandemic has mutated into a human tragedy rather than an economic crisis, and monetary policy is not the right instrument to deal with this.

“…The ill effects of the pandemic are now concentrated in narrow pockets of the economy, and monetary policy is much less effective than fiscal policy for providing targeted relief to the worst affected segments of the economy,” he said.

“…Inflationary pressures are beginning to show signs of greater persistence than anticipated earlier,” the Professor said.

He flagged two other risks – one to inflation (the ongoing transition to green energy worldwide poses a significant risk of creating a series of energy price shocks) and the other to growth (the tail risk to global growth posed by emerging financial sector fragility in China) – are well beyond the control of the MPC, which warrant a heightened degree of flexibility and agility.

Varma opined that a pattern of policy making in slow motion that is guided by an excessive desire to avoid surprises is no longer appropriate.

Views of other members

Shashanka Bhide, Senior Advisor, National Council of Applied Economic Research, Delhi, noted that in the context of the uncertainties in the external demand and price conditions and an uneven sectoral growth pattern, an accommodative monetary policy stance and broader policy support are necessary at this juncture for strengthening the growth momentum and reducing inflation pressures.

Ashima Goyal, Emeritus Professor, Indira Gandhi Institute of Development Research, Mumbai, observed that global price shocks have turned out to be more persistent, contributing to sticky core inflation.

She emphasised that tax cuts on petroleum products are essential to break the upward movement that could impart persistence to domestic inflation.

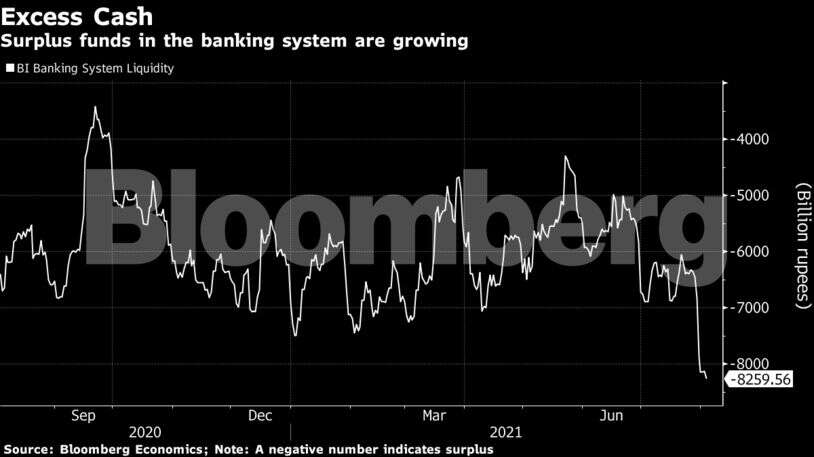

Goyal felt that liquidity needs to be kept in sufficient surplus to absorb large shocks from foreign flows, government cash balances and currency leakages even as the excess is reduced allowing the reverse repo to rise gradually and arrangements for non-banks remain in place.

She suggested that a higher fixed reverse repo rate for banks could be linked to raising their interest rates on deposit accounts.

‘Close watch needed’

MD Patra, Deputy Governor, RBI, said even as domestic macroeconomic configurations are improving, the risks from global developments are rising and warrant a close watch as they could stifle the recovery that is underway in India.

“…In my view, the biggest risks to India’s macroeconomic prospects are global and they could materialise suddenly,” he cautioned.

Mridul K Saggar, Executive Director, RBI, stated that if at all some guidance is needed at this stage, it has to be a soft one, with the Reserve Bank preparing markets that while policy stance is likely to remain accommodative till growth is revived on a durable basis, liquidity levels will be adjusted dynamically to appropriate lower levels that are still consistent with accommodative stance.

“…In my judgement, if no new disruptions to growth emerge, output gap will close sometime in 2022-23 and monetary policy should start to gradually reposition to lowering underlying inflation and inflation expectations next year, especially if inflation edges up from the energy and services side amid sticky goods core inflation,” Saggar said.

[ad_2]