The domestic equity market was in a cheerful mood on Friday as the Reserve Bank of India’s Monetary Policy Committee decided to maintain status quo on key policy rates and retain an “accommodative” stance till evidence of durable growth appears.

It was RBI Governor Das’s comments on the future course of monetary policy action, ramping up of economic growth and elevated inflation that cheered investors.

The benchmark indices extended rally for second consecutive session on Friday, and as a result the market closed higher in four out of five sessions this week.

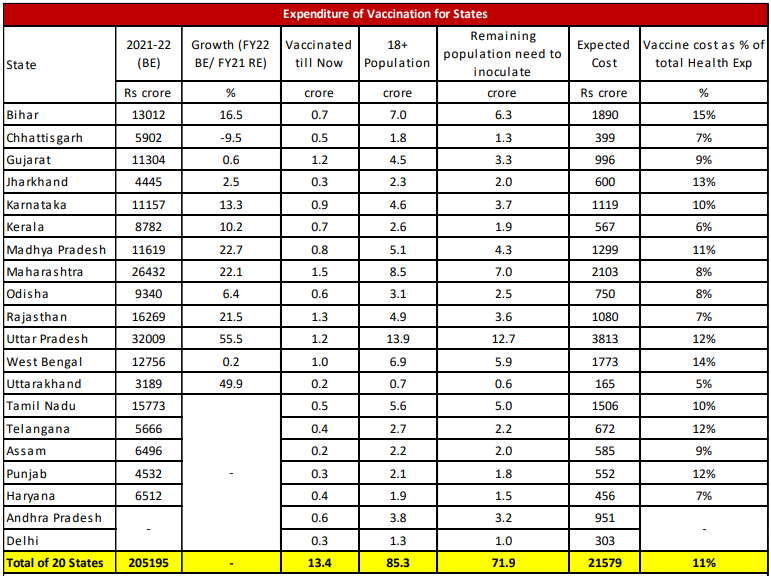

Festival demand outlook, RBI monetary policy, Q2 earnings data backed by recovery in economic activity, US President’s recovery, weak cues from Asian markets, Evergrande crisis, developments around US economy and strong vaccination numbers were key driving factors this week.

Monday Closing bell: Benchmark indices snap four-day losing streak, end almost 1% higher each

Dalal Street staged a strong comeback on Monday, recouping some of last week’s losses, as benchmark indices each ended almost 1% higher. At close, the Sensex and Nifty50 were up 0.91% at 59299 and 17691, respectively.

The broader markets, too, ended the day in the positive territory, with the BSE Midcap gaining 1.51% and BSE Smallcap 1.71%.

The Nifty PSU Banks outperformed gaining 2.10%, the Nifty Bank ended 0.95% higher at 37,579, and the Nifty Financial Services ended 0.96% higher at 18,312. Bajaj Finserv, SBI and Bajaj Finance were among the top gainers.

Tuesday Closing bell: Indices volatile, each end nearly 1% higher

Domestic equity indices started the day flat with negative bias but bulls asserted control as the day progressed, forcing headline indices to surge higher. S&P BSE Sensex closed 0.75% higher at 59,744, while the Nifty50 jumped 0.74% to end at 17,822.

The broader markets underperformed, with the Midcap index almost unchanged and Smallcap index ending with gains of 0.4%.

After a volatile session, the Nifty PSU Bank index ended 0.44% lower at 2,542 points, breaking its six-day winning streak. The Nifty Bank gained 0.43% to close at 37,741, while Nifty Financial Services ended 0.30% higher at 18,367. IndusInd Bank soared 5% to end as the top Sensex gainer, while Bajaj Finance and Bajaj Finserv were among the top laggards.

Wednesday Closing bell : Benchmark indices fell 1% amid weak global cues

Domestic benchmark indices traded with gains most of Wednesday but failed to sustain the highs and closed deep in the red. At close, the Sensex was down 0.93% at 59,189 and the Nifty was down 0.99% at 17,646.

Broader markets were also volatile, with BSE Midcap index falling 0.5% and Smallcap index ending with more than 1% loss.

The Nifty PSU Bank highly underperformed the day, losing 1.94%, while Nifty Bank slipped 0.58% ending at 37,521. Nifty Financial Services closed 0.32% lower at 18,309.

Only three of thirty Sensex constituents closed with gains. HDFC Bank was the top gainer, jumping 1.24%, followed by Bajaj Finance and HDFC. Deep down in red was IndusInd Bank, down over 3%.

Thursday Closing bell: Nifty ends near 17,800, Sensex jumps 0.80% ahead of RBI policy

The Nifty had a sharp bounce after a steep decline the previous day. After opening in the green, Nifty maintained the lead and closed with a gain of 0.85% at 17,796, while Sensex ended the day with a gain of 0.80% at 59,667.

Except oil and gas, all other sectoral indices ended in the green, the BSE midcap and smallcap indices outperformed adding over 1% each.

The Nifty PSU Bank Index recovered from the previous day’s losses to end 0.64% higher at 2508. Nifty Bank was able to end above the 37,700-mark, gaining 0.62% to close at 37,753, while Nifty Financial Services closed 0.15% flat with positive bias at 18,336. Induslnd Bank made its way back among the top gainers, while HDFC was among the worst performing Sensex constituents.

Friday Closing Bell: Sensex ends above 60,000 post RBI MPC meet outcome

Benchmark indices ended over half a percent higher each on Friday as investors cheered the outcome of the RBI MPC meet. BSE Sensex ended 0.64% up at 60,059, while the NSE Nifty 50 settled at 17,895, up 0.59%.

The Nifty PSU Banks outperformed and soared 1.65% to end at 2,550. The Nifty Bank ended flat, with a positive bias at 37,755, up 0.06%, while the Nifty Financial Services index ended in the red at 18,289, down 0.34%. Piramal Enterprises was the worst performing Sensex stock, down more than 5%, followed by ICICI Prudential and Kotak Mahindra Bank. Axis Bank and Bajaj Finserv were among top gainers.

Key Takeaways

RBI keeps key policy rates unchanged in Oct MPC meet

The Reserve Bank of India today decided to maintain status quo on key policy rates, for the eighth time in a row, in its bi-monthly Monetary Policy Committee meeting.

The repo rate remains unchanged at 4%, while the reverse repo rate at 3.35%. The central bank also decided to maintain accommodative stance.The central bank has also kept the MSF and bank rates steady at 4.25 percent.

The central bank has cut CPI inflation forecast for FY22 to 5.3 percent from 5.7 percent, while it has retained FY22 GDP growth forecast at 9.5 percent.

For Q2FY22, RBI expects GDP at 7.9 percent, up from 7.3% earlier, for Q3 , at 6.8%, up from 6.3%, while for Q4 and Q1FY23, RBI has retained its projection of 6.1% and 17.2%, respectively.

For CPI inflation, RBI expects 5.1%, from 5.9% earlier in Q2, while 4.5% from 5.3% in Q3, and retained the projection at 5.8% for Q4. For the first quarter of FY23, RBI sees CPI at 5.2%, up from 5.1% projected earlier.

Life insurance companies poised for strong Q2

Indian life insurance companies are poised to post up to 34% growth in the value of premiums, paced by higher volumes, group insurance coverage and sale of fixed-income linked coverage products.

However, margin expansion could be restrained due to a rise in reinsurance rates. Analysts are also monitoring residual Covid-linked claims in the second quarter after a sharp jump in the first quarter that led to a rise in provisions.

Elara Securities expects the top four life insurers – HDFC Life, ICICI Prudential Life, Max Life and SBI Life – to post an annualised premium equivalent (APE) growth of between 14% and 34% in the second quarter.

RBI moves NCLT against SREI Equipment Finance and SREI Infra

The Reserve Bank of India has taken the Srei Infrastructure Finance and Srei Equipment Finance to the National Company Law Tribunal’s Kolkata bench on Friday, a day after the Bombay High Court rejected a writ petition by Srei group promoter Hemant Kanoria against the central bank move to supersede the boards of the company.

This is on expected line as the central bank had announced on October 4 that it would take steps to refer the Srei case to the bankruptcy court.

Govt may allow 20% foreign investment in LIC IPO

India is considering a proposal for foreign investors to own as much as 20% in Life Insurance Corporation, according to a person with knowledge of the matter, which would enable them to participate in the nation’s biggest initial public offering.

Under discussion is a plan to amend FDI rules so that investors can pick up the stake without the government’s approval under the so-called automatic route, the person said, asking not to be identified as the deliberations are private.

While FDI of as much as 74% is permitted in most Indian insurers, the rules don’t apply to LIC because it is a special entity created by an act of parliament.

Insurers can maintain current a/cs in appropriate number of banks: Irdai

Insurance regulator Irdai on Wednesday said insurers can maintain current accounts in an appropriate number of banks for premium collection and policy payments for the convenience of policyholders and ease of doing business. Insurance Regulatory and Development Authority of India (Irdai) has issued the clarification in the backdrop of the RBI’s circular on “Opening of Current Accounts by Banks – Need for Discipline”.

In the August 2020 circular, the RBI had instructed banks not to open current accounts for customers who have availed of credit facilities in the form of cash credit (CC) / overdraft (OD) from the banking system.

Moody’s affirms ratings of 9 Indian Banks, changes outlook to stable

Global rating firm Moody’s on 6 October, affirmed the long-term local and foreign current deposit ratings of Axis Bank, HDFC Bank, ICICI and State Bank of India at Baa3, following sovereign rating action. At the same time, their rating outlooks have been changed to stable from negative.

This rating action is driven by Moody’s recent affirmation of the Indian government’s Baa3 issuer rating and change in outlook to stable from negative.

Moody’s also affirmed the long-term local and foreign currency deposit ratings of Bank of Baroda, Canara Bank, Punjab National Bank and Union Bank of India. The rating outlooks of these banks has also been changed to stable from negative.

SBI also cast doubt on the criticism that elections were responsible for faster spread of the virus. Many analysts and epidemiologists believe that the elections were one of the major factors behind the record cases in election states.

SBI also cast doubt on the criticism that elections were responsible for faster spread of the virus. Many analysts and epidemiologists believe that the elections were one of the major factors behind the record cases in election states.