Axis Bank has paid Rs 41.4 lakh to Sebi to settle its case of non-disclosure of information relating to offloading of the bank’s shares by its promoter United India Insurance Company(UIIC).

The non-life insurer also paid Rs 10.1 lakh to the regulator to settle the same case.

Sebi said it noted in the investigation that during the period from October 01, 2017 to September 30, 2018, the value of trades by UICC in the securities of the private lender on each trading day was more than Rs 10 lakh.

Under Sebi rules, Axis Bank was required to disclose the same to the stock exchange within two trading days of the receipt of the disclosure from UIIC.

“However, the same was disclosed by the applicant (Axis Bank) to the stock exchange only on October 16, 2020, only with a delay of 1072 – 1080 days,” Sebi said in its order on Tuesday.

The regulator said in five instances the disclosures made by UIIC to Axis Bank was with a delay of 10-17 days. It was required to disclose the same within two working days.

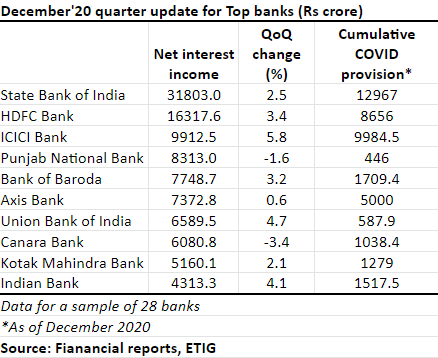

ET Intelligence Group: The aggregate bad loan provisioning by banks fell sequentially for the fourth consecutive quarter in December though some of them increased COVID related provisioning. For a sample of 28 banks, provisioning for bad loans or nonperforming assets (NPA) fell by 27.5% sequentially to Rs 24,149.7 crore in the December quarter. It was the lowest in the seven quarters under observation.

The loan loss provisioning by banks has been benign in the current fiscal year so far on account of various schemes launched by the central bank to reduce the impact of the pandemic. “Bank NPAs this year would tend to be a bit nebulous given the various forbearance dispensations that have been made besides the restructuring schemes that have been introduced,” noted CARE Ratings in a report.

A majority of the sample banks, 19 to be precise, reported lower NPA provisioning compared with the previous quarter. Among them were public sector banks (PSBs) including State Bank of India (SBI), Punjab National Bank (PNB), Union Bank, Indian Bank and Canara Bank and their private sector counterparts such as HDFC Bank, ICICI Bank, and IndusInd Bank. These banks recorded a double digit sequential drop in NPA provisions for the December quarter. Banks including Kotak Bank, Axis Bank, and Yes Bank showed a sequential jump in bad loan provisioning.

The sample’s COVID-19 provisioning increased by 22.7% sequentially to Rs 14,291.1 crore in the December quarter led by a higher provisioning by SBI, HDFC Bank, and ICICI Bank. The sample’s net interest income fell marginally by 1.4% to Rs 1.3 lakh crore.

According to the CARE Ratings report, the gross NPAs of the banking system fell to Rs 7.4 lakh crore in the December quarter from Rs 7.9 lakh crore in the previous quarter while the NPA ratio fell to 7% from 7.7% by similar comparison.

The banking, finance and insurance (BFSI) sector reported a gradual recovery in credit offtake amid buoyant festive demand in the December quarter. “The BFSI sector saw robust operational delivery, especially in the large-cap banks, with above 70% provisioning coverage ratio and minimal restructuring in the loan books,” said Gautam Duggad, rresearch head, Motilal Oswal Institutional Equities.

The debate in Indian banks has quickly shifted from impaired loans to growth. Stocks have done well over the past week to three months and are likely pricing in some growth recovery. Growth momentum is strong, and it is believed that the next leg of returns will be driven by valuation re-rating to much above-average valuations.

According to the report, the balance sheets at large private banks are among the strongest ever post any crisis with strong capital ratios with high non-specific loan provisions and significant liquidity. Loan growth has surprised positively with 70% incremental market share during F9M21. As the economy improves, it is expected to see significant earnings acceleration.

Morgan Stanley raises price targets to factor in 10-15% above-mean valuations at HDFC Bank and Axis Bank. ICICI’s valuation is well above mean levels given significantly higher profitability compared to past levels. A combination of valuation re-rating and strong earnings compounding drives 30-40% upside for the group.

“Our top picks are ICICI, HDFC Bank and Axis Bank. IndusInd Bank should also benefit from the cyclical tailwinds. The questions that we are being asked include why buy the Indian Financial stocks incrementally and can the stocks continue to do well: We believe this cycle is likely to be similar to the one in the early 2000s. Balance sheets at private banks are the best ever in terms of capital, provisions and liquidity. This will help them gain market share at an accelerated pace” said the report.

Profitability is high, helped by strong improvement in loan spreads in recent years as well as lower tax rates. Consequently, return ratios are also expected to reach or cross previous cycle peaks. With strong digital capabilities, and given the different evolution and regulatory dynamics in Large Indian private banks, it is believed that the risks are manageable. Asset quality trends have surprised positively at large private banks Indian Private Banks are exiting the cycle with strong excess provisions and asset quality trends have been much better than expected. Impaired loan formation was expected to pick up as the moratorium ended in August,2020 and restructuring window for corporate and retail loans ended in December, 20.

However, the trends surprised positively – impaired loan formation was 1.8-2.4% in F9M21 Vs 1.7-3.4% in F9M20. While unsecured retail and CV NPL formations have been high, corporate asset quality and secured retail have surprised positively with the stress largely being in disproportionately affected segments CVs, MFI, real estate, travel,etc.

Digital adoption has picked up sharply; will continue to improve: Large private banks have done well on digitization and have improved significantly. Product offerings, where delivery and convenience can match better than that of the fintechs, this has helped them tie up with new players efficiently. Distribution capabilities have improved whereas speed, accessibility and cost of delivery has reduced.

Underwriting practices with new datasets are now originating because of which the ability to underwrite has improved and costs have lowered since.

The fourth largest private sector lender by market capitalisation, Axis Bank has reported a significant 36.4 percent year-on-year (YoY) decline in standalone profit for the quarter ended December 2020 with elevated provisions (up 33 percent YoY).

Net Interest Income (NII) for the quarter rose 14% to Rs 7,373 crore from Rs 6,453 crore in the year-ago quarter. Net interest margin (NIM) for the quarter rose to 3.59% compared with 3.57% in the year-ago quarter

“The bank holds cumulative provisions (standard + additional other than NPA) of Rs 11,856 crore at the end of Q3FY21. It is pertinent to note that this is over and above the NPA provisioning included in our PCR calculations. These cumulative provisions translate to a standard asset coverage of 2.08 per cent as on December 31. On an aggregated basis, our provision coverage ratio stands at 116 per cent,” the bank said

According to the bank’s BSE filing, In the December quarter, the bank reported Gross NPA and net NPA at 3.44% and 0.74% respectively as against 4.18% and 0.98% during the September quarter. The restructured loans as at 31st December, 2020 stood at ₹2,709 crore that translates to 0.42% of the gross customer assets.

According to Puneet Sharma, chief financial officer at Axis Bank, about 83% of the slippages during the quarter came from the retail segment, which included both secured and unsecured accounts. “These are accounts which were under moratorium between March and August..We are expecting the fourth quarter slippages number to improve from the December quarter. We are counting FY22 as a look forward year.”

The rise in slippages from Axis Bank’s retail loan portfolio has led to tightening of credit norms by the bank, especially in the retail book.

Total number of provisions and contingencies for the quarter stood at Rs 4,604.28, which was higher than Rs 4,580.65 crore that it reported in the September quarter and Rs 3,470.92 crore in the year-ago quarter.

Shares of Axis Bank on Thursday declined over 2 per cent in early trade after the company reported a 29 per cent decline in December quarter consolidated net.

The stock opened on a weak note and further dipped 2.35 per cent to ₹617 on the BSE. But it soon bounced back wiping out the early losses and was trading in the green at ₹643.05, registering a gain of 1.76 per cent.

At the NSE also, it opened lower and declined 2.54 per cent to ₹616. In a similar trend, it bounced back as the trade progressed to quote at ₹641.20, up 1.44 per cent.

The country’s third largest private sector lender Axis Bank on Wednesday reported a 29 per cent decline in December quarter consolidated net at ₹1,334 crore, and reported a spike in non-performing assets from the retail assets side. In the 2019 December quarter, consolidated net profit was at ₹1,884 crore.

On a standalone basis, the city-based bank’s net profit for the October-December period declined 36 per cent to ₹1,116 crore from ₹1,757 crore in the same period a year ago. It reported fresh slippages of ₹6,736 crore under the IRAC norms, as against ₹6,214 crore in the year-ago period.

The same had come down to ₹1,572 crore in the preceding September quarter.

A bulk 83 per cent of the fresh slippages came from retail assets, which had become a focus area for lenders across the system in the last few years because of its perceived resilience in face of stress being reported by the corporate segment.

Its operating profit rose 6% YoY to Rs 6,096 crore.

Axis Bank on Wednesday reported a 36% year-on-year (y-o-y) drop in net profit for the December quarter (Q3FY21) to Rs 1,117 crore on higher provisions. The bottom-line was lower than the Bloomberg estimate of Rs 2,760 crore. The bank’s provisions rose 33% YoY to Rs 4,604 crore, but remained flat sequentially. The bank said the profits after tax for the quarter were adversely impacted to the extent of Rs 1,050 crore on account of prudent expenses and provisioning charges. Its operating profit rose 6% YoY to Rs 6,096 crore.

MD and CEO Amitabh Chaudhry said, “We have done provisioning as if Supreme Court standstill on recognising fresh NPAs was not there. As the economy turns around, we see a fresh enthusiasm and positivity returning to both retail and corporate business,” he said. “The sectors like housing, cement and steel have been surprisingly strong, and we expect this momentum to continue,” the MD added.

The net interest income (NII) increased 14% YoY and 2% QoQ to Rs 7,373 crore. The net interest margin (NIM) remained at 3.59%, a jump of 2 basis points (bps) YoY and 1 bps QoQ. The bank has made provisions on accounts more than 90 days past due (90+ DPD), which were not classified as non-performing assets (NPA) pursuant to the SC’s direction. The apex court had earlier directed lenders not to recognise fresh NPAs till further orders in the interest-on-interest case.

Provisioning coverage ratio (PCR) improved to 75% in the third quarter, compared to 60% in the same quarter last year. “On an aggregated basis, our provision coverage ratio stands at 116% gross NPAs,” the bank said.

The asset quality, however, showed an improvement. The gross NPA ratio improved 74 bps to 3.44%, compared to 4.18% in the previous quarter. Similarly, net NPA ratio came down 24 bps to 0.74% from 0.98% in the September quarter. Without SC standstill on declaring fresh NPAs, gross NPA ratio would have been at 4.55% and the net NPA ratio at 1.19%, the bank said.

Gross slippages during the quarter surged to Rs 6,736 crore, compared to Rs 1,572 crore in Q2FY21 and Rs 6,214 crore in Q3FY20. The bank said 85% of the slippages had come from the retail segment. However, the management believes next quarter will be better than the current one.

Puneet Sharma, CFO, Axis Bank, said, “We believe Q4 will be better than Q3 in terms of asset quality.”

Recoveries and upgrades from NPAs during the quarter were at Rs 905 crore, while write-offs were at Rs 4,258 crore. The restructured loans stood at Rs 2,709 crore that translated to 0.42% of the gross customer assets.

The RBI had earlier allowed one-time restructuring for borrowers impacted by Covid-19. Advances during the quarter grew 6% YoY and 1% QoQ to Rs 5.83 lakh crore. The bank also said retail disbursements for the quarter were at all-time highs.

Deposits grew 10.5% YoY and 3% QoQ to Rs 6.54 lakh crore in Q3FY21. Current account savings account (CASA) ratio improved 232 bps YoY and 158 bps QoQ to 42%. The lender’s other income remained flat on a y-o-y and q-o-q basis at Rs 3,776 crore. The fee income, however, showed 5% y-o-y and 6% q-o-q increase to Rs 2,906 crore. The capital adequacy stood at 19.31% at the end of December.

Competition Commission of India (CCI) has approved the stake acquisition in Max Life Insurance Company by Axis Bank, Axis Capital and Axis Securities.

Axis Bank had sought CCI nod to acquire upto 20 per cent stake in Max Life in a deal also involving stake sale to the bank’s subsidiaries Axis Capital and Axis Securities.

It maybe recalled that Axis Bank had to revise its agreement on stake buy in Max Life Insurance as the Reserve Bank of India had rejected this bank’s earlier proposal to directly buy 17 per cent in Max Life Insurance.

As per the combination notice filed with CCI , the shareholding of Axis Bank in Max Life will increase from about 1 per cent to approximately 9.9 per cent.

Also, Axis Capital and Axis Securities will acquire 2 per cent and 1 per cent, respectively, shareholding in Max Life. Axis entities will also have a right to acquire an additional stake of up to 7 per cent in Max Life, in one or more tranches, taking their overall stake to 19.99 per cent.

“Commission approves acquisition of the stake in Max Life Insurance Company by Axis Bank, Axis Capital and Axis Securities,” the competition watchdog said in a tweet.

In December last year, Max Financial Services Limited (MFSL), the parent company of Max Life Insurance, completed a swap of Mitsui Sumitomo Insurance Company’s (MSI) 20.57 per cent stake in Max Life Insurance with 21.87 per cent stake in MFSL.

Post this swap, MFSL’s stake in Max Life effectively increased to 93.10 per cent from 72.5 per cent held earlier.

Named “Aura”, the card would entitle various benefits including offering an annual medical check-up through IndushealthPlus, and four free monthly online consultations through Practo across 21 specialities. Axis Bank said cardholders would also be allowed four free fitness sessions through fitness platform Fitternity, along with access to 16 recorded training sessions.

Sanjeev Moghe, EVP & Head, Cards & Payments, Axis Bank, on the launch of the card said “Our analytics indicated a strong trend amongst consumers with the way they have been spending on health care products, which showed a significant spend lift in the health and wellness categories. To address this specific customer need and to tap the growing market, we have launched ‘AURA’, a credit card loaded with health and wellness solutions.”

“We believe that there is a genuine need of a product catering to the health and wellness needs of customers, and this can be easily addressed through our unique product proposition,” he further added.

Private lender YES Bank had on January 15 launched its health and wellness dedicated credit cards, which include health check-ups, lifestyle benefits and doctor consultations.

Fixed deposits (FDs) are financial instruments provided by banks or NBFCs that offer investors better interest rates than the regular savings accounts. FDs are considered one of the safest investment options and are also called term deposits as they are booked for a fixed term that may range from 7 days to up to 10 years.

Latest rates being offered by some of the top Financial Institutions:

State Bank of India On FDs between 7 days and 45 days, SBI gives 2.9% interest. Between 46 days and 179 days, the interest is 3.9%. FDs of 180 days to less than one year will get you an interest of 4.4%. For deposits with maturity between 1 year and up to 2 years fetch 5% interest. FDs with tenor 3 years to less than 5 years give 5.3%, while those maturing in 5 years and up to 10 years give 5.4 percent.

HDFC Bank On FDs between 7 and 29 days, HDFC Bank gives 2.50% interest. For 30 to 90 days, it is 3.00%. For 91 days to 6 months, the interest rate will be 3.50%. For FDs of 6 months 1 days to 1 day less than a year, the interest is 4.40%. For 1 year it is 4.90%. For 1 year 1 day to 2 years, you can get an interest of 4.90%. For 2 years 1 day to 3 years, the rate is 5.15%. On FDs between 3 year 1 day and 5 years, you can enjoy an interest rate of 5.30%. And FDs maturing between 5 years 1 day and 10 years will fetch you 5.50%.

ICICI Bank On FDs between 7 and 29 days, ICICI Bank gives 2.50% interest. From 30 to 90 days, it is 3.00%. From 91 days to 184 days, the interest rate will be 3.50%. For FDs of 185 to 290 days to less than 1 year, you can get interest of 4.40%. For 1 year to 389 days to 390 days upto 18 months, the rate is 4.90%. On FDs between 18 months upto 2 years, you can enjoy interest rate of 5%. From 2 years 1 day upto 3 years, the interest rate is 5.15%, whereas for 3 years 1 day upto 5 years it is 5.35%. For 5 years 1 day to 10 years, the interest rate is 5.50%.

Axis Bank For Axis Bank, the FDs between 7 and 29 days is 2.50%, and from 30 days to 3 months it is 3.00%. From 3 months to 4 months interest rate is 3.50%, 4 months to 6 months interest rate will be 3.75%, and from 6 months upto 11 months and 25 days it will be 4.40%. For FDs from 11 months and 25 days upto 1 year 5 days it is 5.15%. On FDs between 1 year 5 days and upto 18 months the interest rate will be 5.10% whereas from 18 months upto 2 years it will be 5.25%. From 2 years upto 5 years the interest rate on FDs is 5.40% and 5.50% from FDs for 5 to 10 years.

Kotak Bank For Kotak Bank, the FDs between 7 to 30 days is 2.50%, and from 31 to 90 days it is 2.75%. From 91 to 179 days the FD interest rate is 3.25% and from 180 to 364 days it is 4.40%. For FDs between 365 to 389 days the rate is 4.50%. From 390 to 391 days it is 4.75% whereas it is 4.75% from 23 months to 23 months and 1 day less than 2 years also. From 3 to 5 years it is again 4.75%. From 5 to 10 years it is 4.50%.

Senior citizen FD rates FD interest rates vary from bank to bank depending on their tenure, amount, and type of depositor. Senior citizens, who are above 60 years, get special interest rates on their fixed deposits, which are often 0.5% above the prevailing interest rates.

Timely closure Timely closure refers to closing the fixed deposit account at the time of its maturity only. When closed upon maturity date, the bank pays back the principal amount with the interest accrued over the tenure chosen.

Premature withdrawal Premature withdrawal or breaking of FD is usually discouraged by lenders, and in such a case they levy a penalty along with paying back the principal amount and interest at a lower rate. However, in case of emergencies, certain banks do waive off the penalty.

The project is part of the bank’s philosophy of a combination of assets and liabilities coming together with technology to ensure that it becomes a significant player in these markets.

Axis Bank is working to deepen its presence across the country’s rural regions with what it calls its ‘deep geo strategy’. This will involve the identification of key branches and dovetailing those to help the bank’s growth, said a senior executive.

Sumit Bali, president and head, retail lending and payments, Axis Bank, said that as part of the deep geo strategy, the lender has identified some of the rural and semi-urban markets where it will have an asset-led strategy to scale up its banking assets and liabilities.

“As part of this initiative we identified about a third of our branches — 1,577 branches — where we’ve launched this asset-led strategy. “It has taken very good shape. Disbursements are up about 26% year-on-year, and growth continues to be pretty strong,” Bali said during an online press conference.

The project is part of the bank’s philosophy of a combination of assets and liabilities coming together with technology to ensure that it becomes a significant player in these markets.

“This is an identified strategy that we want to be a significant player in the rural part of the country and we’ve also made a strategic investment in the CSC (common service centres), which will help us set up a strong distribution footprint across the country,” Bali said.

Axis Bank has already identified close to 5,000 village-level entrepreneurs as distribution points across the country. It is using these branches to distribute its asset products, such as farmer funding, gold loans, small business banking, home loans and two-wheeler loans. Eighty eight percent of the loans originated under the project are secured loans.

“We are very excited with this initiative going forward and we see strong growth month-on-month and this will, therefore, also help us become a significant strategic player in the overall rural side of the country. “It will also generate for us priority-sector and agri assets, going forward,” Bali said.