Nearly five years since launch, the Stand-up India scheme has seen loans sanctioned by banks in aggregate of ₹ 25,586 crore to over 1,14,322 accounts, the Finance Ministry said on Sunday.

This scheme was launched on April 5, 2016 to promote entrepreneurship amongst women, Scheduled Castes and Scheduled Tribes category.

While the total loans sanctioned to women stood at ₹ 21,200.77 crore (93034 accounts); the loans sanctioned to SCs stood at ₹ 3335.87 crore (16258 accounts) and STs at ₹1049.72 crore (4,970 accounts), an official release said.

The main purpose of Stand-up India scheme— which is now extended upto the year 2025– is to provide loans for setting up greenfield enterprises in manufacturing, services or the trading sector and activities allied to agriculture by both ready and trainee borrowers.

This scheme facilitates bank loans between ₹ 10 lakhs to ₹ 1 crore to atleast one scheduled caste/scheduled tribe borrower and atleast one woman borrower per bank branch of scheduled commercial banks.

Loans under this scheme are available for only greenfield projects. Greenfield signifies, in this context, the first time venture of the beneficiary in the manufacturing, services or the trading sector and activities allied to agriculture.

Public sector banks may have to bear a burden of Rs 1,800-2,000 crore arising due to a recent Supreme Court judgement on the waiver of compound interest on all loan accounts which opted for moratorium during March-August 2020, sources said.

The judgement covers loans above Rs 2 crore as loans below this got blanket interest on interest waiver in November last year. Compound interest support scheme for loan moratorium cost the government Rs 5,500 crore during 2020-21 and the scheme covered all borrowers including the prompt one who did not avail moratorium.

According to banking sources, initially 60 per cent of borrowers availed moratorium and gradually the percentage came down to 40 per cent and even less as collection improved with ease in lockdown. In case of corporate, this was as low as 25 per cent as far as public sector banks were concerned.

They further said, banks would provide compound interest waiver for the period a borrower had availed moratorium. For example, if a borrower availed moratorium of three months, the waiver would be for that period.

The Reserve Bank of India (RBI) on March 27 last year announced a loan moratorium on payment of instalments of term loans falling due between March 1 and May 31, 2020, due to the pandemic, later the same was extended to August 31.

The apex court order this time is only limited to those who availed moratorium so the liability of the public sector bank should be less than Rs 2,000 crore as per rough calculations, sources added.

Besides, they said, the order does not specify a timeframe for the settlement of compound interest unlike last time so banks can devise a mechanism of adjusting or settling it in staggered manner.

Meanwhile, Indian Banks’ Association (IBA) has written to the government to compensate lenders for interest on interest waiver.

The government would take a call depending on various considerations.

The Supreme Court last month directed that no compound or penal interest shall be charged from borrowers for the six-month loan moratorium period, which was announced last year amid the Covid-19 pandemic, and the amount already charged shall be refunded, credited or adjusted.

The apex court refused to interfere with the Centre and RBI’s decision to not extend the loan moratorium beyond August 31 last year, saying it is a policy decision.

Rejecting pleas for a complete waiver on interest the court opined that such a move would have consequences on the economy. The bench also said that interest waiver would affect depositors. Along with this, the court also rejected pleas for further relief in the matter.

In a clear signal that soft interest cycle for home loan borrowers is over, State Bank of India (SBI) has hiked the minimum interest rate on home loans by 25 basis points (bps) from 6.70 per cent to 6.95 per cent with effect from April 1, 2021.

This hike in minimum home loan rate by SBI will prompt other lenders to follow suit.

SBI had lowered the minimum interest rate from 6.80 per cent to 6.70 per cent on March 1, 2021 for a limited period up to March 31, 2021.

The Bank will also charge a consolidated processing fee. This will be 0.40 per cent of the loan amount plus applicable GST, subject to a minimum of ₹10,000 and maximum of ₹30,000 plus GST.

However, for builder tie-up projects where individual TIR (title investigation report) and valuation is not required, the processingaforementioned fee will be 0.40 per cent of loan amount subject to maximum recovery of ₹10,000 plus applicable tax. And, if TIR and Valuation is required, then normal charge will be applicable., as per the Bank’s website.

The lender had waived home loan processing fees till March 31, 2021.

In February, the Bank said it expects to double its home loan portfolio in the next five years to Rs ₹10 lakh crore on the back of higher economic growth and growing preference of the new generation to buy a home early.

SBI took about 10 years to grow its home loan portfolio from ₹89,000 crore in FY2011 to touch the ₹5 lakh crore mark, Chairman Dinesh Kumar Khara told media in February 2021.

SBI took about 10 years to grow its home loan portfolio from ₹89,000 crore in FY2011 to touch the ₹5 lakh crore mark, Chairman Dinesh Kumar Khara told media at a press meet in February 2021.

UPI transaction value witnessed a growth of 18.7 per cent month-on-month to Rs 5.05 lakh crore in March 2021 from Rs 4.25 lakh crore in February 2021.

Amid Covid, India was home to the highest number of real-time online transactions in 2020 ahead of countries such as China and the US. 25.5 billion real-time payments transactions were processed in the country followed by 15.7 billion in China, 6 billion in South Korea, 5.2 billion in Thailand, and 2.8 billion in the UK. Among the top 10 countries, the US was ranked ninth with 1.2 billion transactions. The transaction volume share for instant payments India, among real-time transactions, was 15.6 per cent and 22.9 per cent for other electronic payments in 2020, according to a report by the UK-based payments system company ACI Worldwide. Importantly, paper-based payments continued to have a considerable share of 61.4 percent in India.

However, this is expected to change by 2025 as volume shares for instant payments and other electronic payments are likely to grow to 37.1 per cent and 34.6 per cent respectively. Consequently, the share of paper-based transactions would contract to 28.3 per cent. Moreover, the share of real-time payments volume in overall electronic transactions will exceed 50 per cent by 2024. “India’s journey of creating a digital financial infrastructure has been characterized by collaboration between the government, the regulator, banks, and fintechs. This has helped to advance the country’s goal of enabling financial inclusion and also provided rapid payments digitization for citizens,” said Kaushik Roy, VP and head of product management, Asia, ME and Africa, ACI Worldwide in a statement.

India’s digital payments market led by Paytm, PhonePe, Pine Labs, Razorpay, BharatPe, and others on the B2C and B2B sides has surged during the pandemic even as incentives such as cash backs, rewards, and offers have helped businesses to attract more customers. Moreover, policy frameworks such as Pre-Paid Instruments (PPI), Universal Payment Interface (UPI) by the NPCI apart from Aadhar, and the launch of BHIM-app have driven the financial inclusion and improved the payment acceptance infrastructure in the country in the past few years.

According to another report by the Indian Private Equity and Venture Capital Association (IVCA) and Ernst & Young, digital payments in India is expected to grow at 27 per cent CAGR during the FY20-25 period from Rs 2,153 lakh crore transactions in FY20 to Rs 7,092 lakh crore in FY25. UPI transaction value witnessed a growth of 18.7 per cent month-on-month to Rs 5.05 lakh crore in March 2021 from Rs 4.25 lakh crore in February 2021 while transaction volume rose by 19 per cent to 2,731.68 million from 2,292.90 million during the said period, according to data released by National Payments Corporation of India (NPCI).

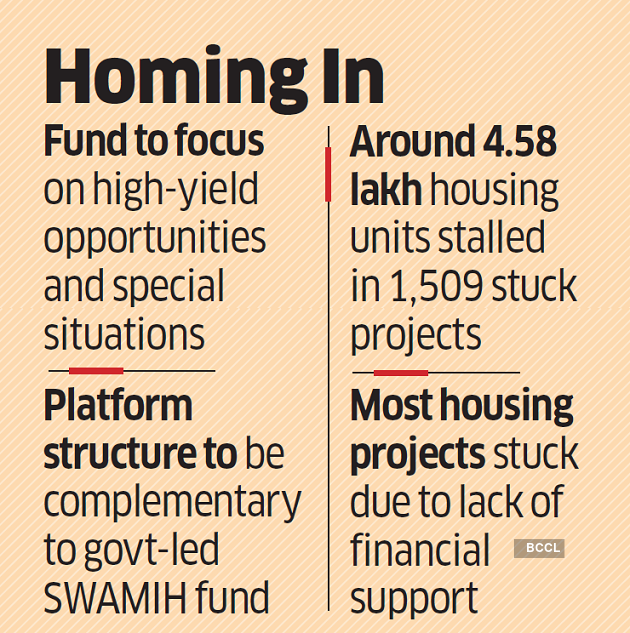

HDFC Capital and global alternative investment major Cerberus Capital Management LP have formed a partnership to create a fund that will focus on high-yield opportunities in Indian residential real estate. The size of the proposed fund will be upwards of $1 billion, said people familiar with the development.

The fund, to be set up through an affiliate of New York-headquartered Cerberus Capital, will target stressed projects, purchase inventory and provide last-mile funding for under-construction residential projects.

“Housing is an integral part of our economy and because of its linkages to other industries and to the labour market, it is a critical sector for ensuring economic growth,” Deepak Parekh, chairman of Housing Development Finance Corporation (HDFC), of which HDFC Capital is a subsidiary, told ET.

The deal is another sign of foreign investment firms’ growing interest in India. “Despite the massive need for housing in the country, a large number of launched projects are in distress, leading to a complete standstill in execution,” said Parekh. “This platform will provide much-needed financing for housing projects and help in delivery of finished units to home buyers.” HDFC and Cerberus declined to comment on the size of the proposed fund.

Currently, the government-backed Special Window for Completion of Construction of Affordable and Mid-Income Housing (SWAMIH) projects is the only large dedicated federal financing pipeline for such projects.

Allow partial exit to lenders

“The structure of the HDFC-Cerberus fund will make it complementary to the government-led SWAMIH fund, as it will also allow partial exit for existing lenders of the project, thereby increasing the scope of projects that can be covered for resolution,” said Vipul Roongta, managing director, HDFC Capital. While HDFC and other financial institutions have invested in SWAMIH fund, the HDFC-Cerberus fund will be the only private sector initiative with an objective of resolving the issue of stuck and distressed housing projects.

“Cerberus has a long track record of partnering with businesses and properties around the world,” said Frank Bruno, co-chief executive, Cerberus. “We are able to provide tailored solutions in sectors with dislocated funding channels in various forms, such as the purchase of assets, creation of operating and lending platforms, and provision of structured capital to best-in-class operators.”

Cerberus has been active in India since 2019 across verticals including acquisition of non-performing assets, provision of capital to corporates and creation of financial services and real estate platforms.

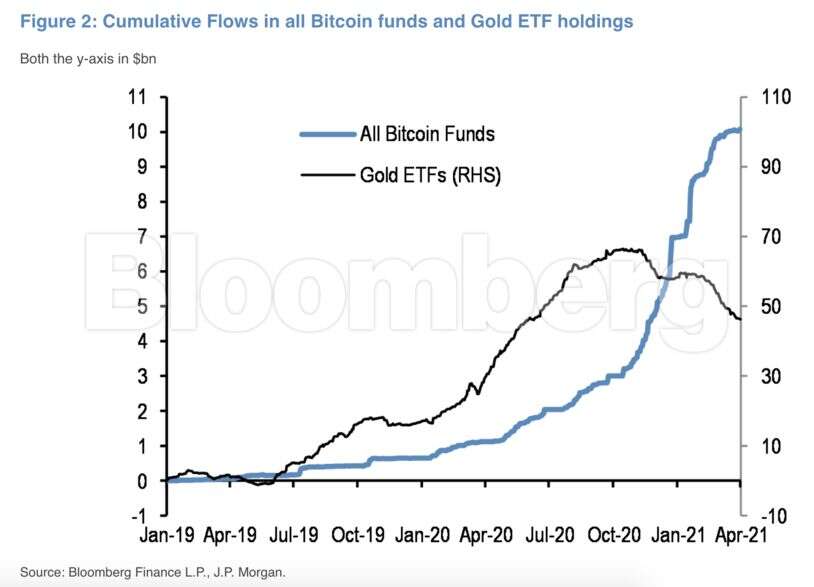

The recent pullback in Bitcoin’s volatility is setting the stage for a trend that could encourage institutions to dive in, according to JPMorgan Chase & Co.

“These tentative signs of Bitcoin volatility normalization are encouraging,” strategists including Nikolaos Panigirtzoglou wrote in report emailed Thursday. “In our opinion, a potential normalization of Bitcoin volatility from here would likely help to reinvigorate the institutional interest going forward.”

Three-month realized volatility for the cryptocurrency has fallen to 86% after rising above 90% in February, they wrote. The six-month measure appears to be stabilizing at around 73%. As volatility subsides, a greater number of institutions could warm to the crypto space, the strategists said.

The coin’s volatility has kept institutions away, something that’s been a key consideration for risk management — the higher the volatility of an asset, the higher the risk capital consumed by it, according to the strategists. None of the biggest U.S. banks right now provide direct access to Bitcoin and its counterparts.

Still, traditional Wall Street firms have been taking a greater interest in the coin, especially after it doubled this year on the heels of a 300% jump in 2020.

Goldman Sachs Group Inc. said this week it’s close to offering investment vehicles for Bitcoin and other digital assets to private wealth clients. Morgan Stanley plans to give rich clients access to three funds that will enable ownership of crypto and Bank of New York Mellon Corp. is developing a platform for traditional and digital assets.

Some of the attention on Bitcoin over the past two quarters has come at the expense of gold, JPMorgan’s strategists said, citing $7 billion of inflows into Bitcoin funds and $20 billion of outflows from exchange-traded funds tracking the precious metal.

Meanwhile, an additional boost to future adoption by institutions could arise from recent changes in Bitcoin’s correlation structure relative to other, traditional assets, according to JPMorgan strategists. These correlations have shifted lower in recent months, “making Bitcoin a more attractive option for multi-asset portfolios for diversification point of view and less vulnerable to any further appreciation in the dollar,” they wrote.

Karnataka Bank has targeted 12 per cent business growth in the current fiscal year, expecting total business of over Rs 1.42 lakh crore.

The lender also said digital banking is the way forward and it is at the cusp of engineering a breakthrough in banking industry as ground has been already laid to be the ‘Digital Bank of the Future’.

Even before the COVID-19 outbreak, the Indian banking industry had been undergoing a paradigm shift from traditional ways of banking with digital technology powering this change, its Managing Director and CEO Mahabaleshwara M S said.

He was speaking to all the staff members and branches across the country virtually on the first day of the current fiscal year (April 1), presenting a broad outline of business goals and strategies for FY22.

The CASA (current account savings account) share of the bank has reached a new high of 31 per cent and the digital transactions have also crossed 90 per cent, the bank said in a release.

“For the new financial year the bank has planned to grow its business at a moderate 12 per cent to take the total business turnover to Rs 1,42,500 crore.

“With a healthy business growth, ‘cost lite’ liability portfolio, strengthened fundamentals etc, the year 2021-22 should be an year of excellence for Karnataka Bank,” Mahabaleshwara said on Thursday.

The advent of payments banks and fintech lenders has accelerated the change in the banking industry and Karnataka Bank took a proactive step in 2017 by initiating a holistic transformation journey ‘Project KBL VIKAAS’, said the lender.

The objective of this journey, founded on digital technology as enabler, is to strengthen the bank’s fundamentals and build long term capabilities to continue to stay ahead of the curve, it added.

The bank has taken many digital initiatives, from establishing a state-of-the-art Digital Centre of Excellence (DCoE) in Bengaluru — a digital innovation hub powering various digital products, to digital loans sanctioning for most of retail products as well as introducing tab banking and web banking for opening savings accounts.

“As the digital is the way forward, we have placed digital banking on fast forward mode to pursue the concept of ‘KBL NxT’.

“With many more digital products lined up for this new financial year under this new set up, Karnataka Bank has a business advantage heading into the new FY 21-22 in a post COVID-19 scenario,” Mahabaleshwara said.

Banks and non-banking finance companies have started increasing deposit rates across tenures, especially rates on longer-term FDs on likely recovery in credit demand and rising inflation.

The number of lenders offering higher rates may go up over the next few months.

Mortgage lender HDFC has increased rates on fixed deposits maturing between 33 and 99 months by 10-25 basis points for the first time in 29 months. HDFC said from March 30, fixed deposits of 33-month duration will fetch 6.2% annualised returns while fixed deposits with 66-month maturity will now fetch 6.6% interest rate and the 99-month deposits will receive 6.65% interest rate. Further, senior citizens would get 0.25% more on the above-mentioned rates. Worth mentioning here is that this is the first time after October 2018 that HDFC Ltd has raised deposit rates. In February, Bajaj Finance, another top-rated lender had raised interest rates on fixed deposits by 40 basis points. Fixed deposits from Bajaj Finance with tenures of three to five years earn 7%.

Negative rate prospects

The finance ministry gave a scare of a rate cut on small savings schemes as such a move would have put pressure on reduction in bank deposit rates.

With inflation above 5%, deposit rates are already threatening to veer into negative territory, any rate cut would be a double whammy for depositors.

Retail depositors have struggled during the pandemic to maintain their earnings and also ensure inflation doesn’t erode their savings.

If inflation continues to rise, banks will have to offer higher deposit rates to investors, who in sight of negative returns, may shift their money elsewhere.

Rates kept down

In 2020, due to the pandemic, the Reserve Bank of India’s (RBI) adopted an accommodative stance with measures to keep the policy rates down throughout the year. It also announced measures to infuse liquidity in the banking system to be able to provide affordable financing and hence, support economic growth. Extra liquidity also kept interest rates down. The credit offtake was low as banks adopted a cautious stance towards lending across all sectors of the economy, which led to lower rates. Growth this year

However, the banking system’s credit growth will almost double to 10 per cent in 2021-22 on the economic recovery and policy interventions.

The economic growth pegged at 10.5% by RBI for FY21-22 and 12% by foreign rating agencies. From a banks’ credit growth perspective, the agency said the expansion will accelerate by 4-5 percentage points to 9-10 per cent in 2021-22.

The faster credit growth will be led by retail loans, which are expected to grow in mid-teens, while corporate loans, which de-grew during 2020-21, are also likely to show a 5-6 per cent jump. This is expected to be driven by investment demand from infrastructure and real estate sectors as well as the release of pent-up consumer demand, thus resulting in high growth in retail finance.

The growth and demand for credit is likely to push up fixed deposit rates in the next 3-9 months.

RBI measures

Contrary to its accommodative stance, RBI has already reduced its liquidity support to the market with no additional liquidity measures announced in the latest monetary policy review in February 2021. It has withdrawn the 1% Cash Reserve Ratio relaxation for banks and now the CRR must be brought up to 4% in two tranches. A hike in CRR will lead to a reduction in liquidity available with banks which may force them to look out for more funds from retail depositors to meet their credit demand, thus adding another factor that can result in higher deposit rates.

Surendra Rosha, Group general manager & CEO, HSBC India

By Malini Bhupta

HSBC group will invest $6 billion in India, a key market for the group, over the next five years. Surendra Rosha, Group general manager & CEO, HSBC India, tells Malini Bhupta the bank offers a unique proposition to its international customers in India, as also Indian businesses on their needs overseas. Edited excerpts:

The pandemic has been a big disruptor. How has it impacted banking globally? The global economy suffered a severe contraction on account of the pandemic and the banking sector was obviously not immune to it. Of the many things the pandemic led to, most significant was that it forced businesses to think differently and work around constraints to find the way forward. It helped to build up a certain degree of flexibility and resilience in a short span, which might have been difficult in regular times. It also accelerated the move towards all things digital. Our clients across segments increasingly transitioned towards digital adoption. This ensured that our servicing abilities were not compromised on account of the lockdown and social distancing. I believe that a substantial part of our banking activities could eventually move towards digital, self-serve models.

The pandemic also resulted in a greater focus on global supply chains and supply chain resilience became a key metric for many management teams and boards. The reshaping of global supply chains also brought into sharp focus India’s role in global manufacturing. Even prior to the pandemic, we had been actively engaging with the Government of India on the reform initiatives, as also to understand how ecosystems and supply chains are evolving. This has helped unearth sectors with growth potential, where we can help nurture the ecosystem. We aim to play a pivotal role in supporting anchor corporates and their suppliers’ ecosystem to strengthen their supply chains, including exploring (and executing) the transition to India.

India is an important market for most global banks with a presence in India. What is your plan for India over the next few years? India is a key component of the HSBC Group’s growth story. In the Group’s annual financial results announced recently, HSBC India recorded a PBT of over $1 billion, that too in a challenging year. HSBC India is currently the third largest contributor to the Group’s profits. Our global network is the core strength of the bank. We aim to continue strengthening the linkages between our global customers and their India needs, just as we seek to serve Indian customers on their global needs. Transaction banking, covering cash management, custody, trade and foreign exchange, is a focus area for us. While the pandemic disrupted global trade, we believe the trade is poised to grow, with India deepening its trade linkages post the pandemic. On the retail side, India has one of the largest diaspora of all and many of its members have banking needs in India. Our ability to connect those who live, work or study across our other markets, back to India makes for quite a unique proposition. Also very important is India’s increasing capital needs and its growing share in global investor portfolios. We serve these investor clients, be they pension funds, sovereign wealth funds, or insurance companies across many markets and will continue to meet their India needs.

Fintechs are set to challenge banks like never before, resulting in many banks partnering with them and even investing in them. How do you see the role of banks changing in times to come? The emergence of fintechs over the last few years has been good for the banking sector. They have brought a sense of urgency to the digital agenda in financial services. Innovation has become a central area of focus for us and many of our peers. We believe there is a tremendous opportunity for banks to partner with fintechs in specific segments. Such a collaborative approach will be good for the larger banking ecosystem. We have worked with fintech partners in the recent past, in the areas of transaction banking and retail banking. We will continue to do so in the coming years, collaborating in segments where we see opportunities to work together.

Digitisation is the new buzzword, with the pandemic accelerating the pace of the phenomenon. How is HSBC responding to the new normal? What about the challenges posed by digitisation, like the rising number of cyber-attacks? The pandemic certainly helped in greater adoption of digital banking channels. At HSBC, however, digital evolution has been an ongoing endeavour. We have been at the forefront of the digital payments ecosystem as well as trade finance, pioneering the adoption of blockchain technology. While digitisation has led to a greater number of online frauds and cyber-attacks, we have been constantly testing our systems and capabilities against malware and cyber-attacks. We are investing in security systems and periodically upgrading our offerings to ensure our customers are secure against cyber-attacks and malware.

Which segments in India are you most excited about as a global bank? And what are you doing to grow in them? We have three lines of business – global banking and markets, commercial banking and wealth and personal banking. Our growth imperatives for all the three lines of business are well articulated. As an international bank, our global network straddles key economic corridors. This means we are uniquely placed to support the needs of our clients and help bolster international trade.

One of the areas I’m most excited about is the emergence of sustainable financing and the growth in renewables. We believe businesses have a great opportunity to help address ecological concerns and areas like climate change need solid strategy, expertise and fast delivery. Globally, the HSBC Group is committing between $750 bn to $1 trn over the next nine years to help businesses reduce their carbon footprint. We will thus be keen to support Indian businesses in this journey.

With globalisation having come under a cloud, do you see the movement of capital being impacted? The pandemic certainly had an impact on globalisation and international trade. It changed the contours of international trade as supply chains were severely disrupted. However, from a long-term perspective, I’m confident international trade will continue to thrive; we’re already seeing the first signs of revival. This will throw up new opportunities as well as challenges for different countries. But the undertying reasons for international trade, for movement of capital, and the larger need for an integrated global economy will certainly not diminish.

From an India standpoint, as the reforms of the last 18 months take hold and it makes a serious push for privatisation, I see India’s share of global trade in goods and services increasing materially over the next five to seven years. Similarly, international capital will play a key role in funding India’s ambitions to build infrastructure and manufacturing capacity.

HSBC is stepping up investments in Asia. What is the plan for India? Asia has always been a core engine of growth for the Group. In its financial results announced recently, the Group has outlined investing around $6 bn over the next five years in its Asian operations, including India. India continues to be attractive from a long-term perspective, given its growth rate, demographics and overall digital framework. We believe it will continue to perform well and its international requirements, whether of capital or trade, will grow. We will keep investing in our capabilities to serve our international clients in India, as well as the overseas needs of our Indian customers. Our unique ability to connect across economic corridors is key to our growth ambitions, and makes us positive about our prospects in India.

CSB’s gold loan portfolio has increased 61.05% y-o-y during the last quarter to touch Rs 6,121.34 crore.

CSB Bank’s gold loan portfolio has slowed down in the fourth quarter while overall business has picked up, the bank said in a regulatory filing.

The Thrissur-based lender has reported that its deposits have increased by 21.2% year-on-year (y-o-y) during the fourth quarter, while advances saw an increase of 26.7% for the same period. CSB Bank had earlier reported that it expects its advances to grow by 20-22% this fiscal despite a slowdown in the gold loan growth.

The lender has reported that its deposits stand at Rs 19,140 crore as on March 31, 2021, while CASA stands at Rs 6,161.80 crore and term deposits at Rs 12,978.24 crore.

CSB’s gold loan portfolio has increased 61.05% y-o-y during the last quarter to touch Rs 6,121.34 crore. Sequentially, the gold loan portfolio has only increased by 8.65 % from Rs 5,633.75 crore reported in the third quarter of the current fiscal.

The bank reported a 89% y-o-y increase in its third quarter net profits to Rs 53.05 crore on higher interest and treasury income. The 101-year-old bank opened 101 branches in FY21.

While HDFC and other financial institutions have invested in SWAMIH fund, the HDFC-Cerberus fund will be the only private sector initiative with an objective of resolving the issue of stuck and distressed housing projects.

While HDFC and other financial institutions have invested in SWAMIH fund, the HDFC-Cerberus fund will be the only private sector initiative with an objective of resolving the issue of stuck and distressed housing projects.