Reserve Bank of India – Press Releases

[ad_1]

Read More/Less

Ajit Prasad Press Release: 2021-2022/1097 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

[ad_2]

Get Bank IFSC & MICR codes here.

[ad_1]

Ajit Prasad Press Release: 2021-2022/1097 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

[ad_2]

[ad_1]

My first question is about valuations. Nifty, Sensex both are at lifetime highs. Are valuations stretched? How much of an upside are you seeing for benchmark indices?

There are two aspects to it. I want to summarise and then I will answer your question specifically. Overall on the one year forward earning basis, the market is at around 30-35% premium which is from 18x to 23x. That is the multiple that we are at. However, having said that, there are still some components which are included in benchmark Nifty in recent years like HDFC Life, SBI Life, Shree Cements carry higher P/E multiple than excluded stocks. Hence, a part of the premium has come from there. Further, improved visibility of earnings rebound post second wave of Covid-19 resulted in higher premium for the market and also from the market cap to GDP perspective.

We further note that the spread between G-Sec yield and Nifty earnings yield has gone up to historical average of 190bps, which may be a cause of concern for the near term. Overall though, the markets have run up and from here on, we would probably see another 10% jump towards the fiscal year end. That is something that we see. There could be some corrections along the way, the journey will have some blips but overall whoever is invested probably will see around 10% to 15% from here on a year-to-year basis.

From the perspective of a midcap versus small cap or a large cap; which part do you think right now holds the most value?

It is in the front end. We have seen significant growth in the largecap stocks. But it is going to be more broad-based and the midcap and smallcap stocks will probably continue the momentum given improved visibility of sustained earnings growth. However, in addition to earnings growth, investors must focus on cash flow generation and corporate governance of companies.

There will always be specific stocks and specific opportunities within the indices will probably provide opportunity and corrections will provide an entry level and another opportunity for anyone in retail or anybody who would have not entered so far.

Notably, every bull phase creates some winners, which causes midcaps to turn into largecaps. We already have many examples like Shree Cement, Tata Consumers, Avenue Supermarts, Adani Ports, Divi’s Lab, SBI Cards, among others.

There has been a flurry of IPOs so far in the year. What are the challenges of valuing these new age entrants into the market?

In 2019, from around $2.5 billion in the primary market (which is IPO) to almost $12 billion so far in 2021, it has been a phenomenal journey. LIC and Paytm are among others that could come in this year. So clearly it is a year of fundraising.

A year when a lot of primary activity is happening is very good because that provides risk capital.

The valuations with regards to overall IPOs or more specifically new age companies will probably be the function of what has been expected and what the investment horizon is. Clearly, if one goes for LIC IPO versus the Zomato or Paytm IPO will be on a completely different perspective. While LIC IPO is on today’s base and some growth rate in future, the new age technologies like Paytm or Zomato will probably be more based upon a little longer term.

Whoever is in it for the long haul…these kinds of IPOs will definitely benefit them. However, there are some players who are not for the long term. Probably more conventional IPOs will be better for them.

What is the earnings season telling us so far? Is the financial sector out of the woods in terms of asset quality?

Earnings so far have been decent and hence the markets are doing well. However, input cost inflation turned out to be a key concern for the market in the last couple of days.

With regards to whether the asset quality is out of the woods or not, the financial stability report from RBI says that it may take around four to six quarters for banks or for the lending companies to recover from the complete impact of any recession or any significant event like Covid-19.

So far so good but I would like to keep an eye on this for another couple of quarters at least so that we can see how it is going to pan out but all the policy responses that have been done so far both on the monetary and fiscal space have been supportive.

But we have another couple of quarters to look out for.

We have seen that so far this month the rupee has taken quite a beating because of a combination of factors; we have oil prices, we have the US Fed talking about tapering etc. Some companies like those in the IT space could benefit from this but what are the broader market implications of depreciation of the rupee?

The rupee usually is a function of two main components; one is the internal policies — how are the interest rates and second are the external fund flows and the liquidity in addition to the crude and other commodity prices.

There was an interesting article that says that the option strike in the US is going as far as above $200 for the Brent crude. It is phenomenal to even read that.

Obviously in the near term, crude probably has an upward trajectory till some correction is brought in by OPEC.

There are two key things that are going to play for currency in the near term future; one will be what steps Fed takes to taper or in what form and fashion.

That will probably determine the liquidity flow and that is where the currency play will come.

And the second is how the local interest rates or the domestic interest rates pan out. These two combinations will probably see where the rupee goes from here. Overall, it may be hovering around the range on a bit of a weakening but it is not going to be too much.

It is going to be around the range depending on what Fed does and how the domestic interest rates pan out.

Recently even the Bank of England governor has been talking about tightening monetary policy. The Fed has given a clear timeline that by November, bond purchases will be tapered. In terms of FII flows coming into India, do you think there would be a meaningful impact once all of this starts out in the advanced economies?

As we have seen in the past, tapering in itself does not cause the reverse fund flows. It is more if something is done beyond expectations.

Whatever has already been priced in or already been considered will not cause any impact on the FIIs.

If something is done over and above what has been expected, there may be some impact. However, the good part is that India being a strong story and robust inflow; that will probably offset some of those reversals because of interest rate arbitrage or the currency.

So overall, we do not expect on a more structural basis FPIs or FIIs flows to be reversed.

Yes, there could be some few months here and there, there could be some correction based upon the event but overall we should be okay.

We have been seeing a lot of talk recently about inclusion of India’s bonds in global indices. RBI has been talking about it. Many research reports including big foreign brokerages have been talking about it. Would that be a game changer for Indian financial markets?

I personally believe it will be and if you would have noticed, there was a recent comment by the deputy governor also that inclusion of the Indian bonds in the global indices in a way is a journey towards the capital account convertibility.

That kind of the roadmap that we are heading toward is very transformational for India to have a foreign flow like that. But it comes with its own impact and as long as that has been managed, I it is going to be a big, big plus for a country like India where there will be a debt fund and infrastructure funding and a lot of that positive funds will probably flow in.

We just have to ensure that the ecosystem has been addressed in a way where we are ready for the capital account convertibility which we have been speaking about for a long time.

In the last policy, the RBI kept interest rates unchanged but it stopped its government security acquisition programme and increased the size of its variable rate reverse repos. Some have taken that as a precursor to some degree of normalisation. Do you think that RBI could run the risk of falling behind the curve if it does not do something like a reverse repo hike by December?

I personally do not believe so. Whatever is being done is along the lines of expectation. There are a lot of reports out there that actually forecast when the interest rate cycle by the central bank will start normalising to pre-Covid level.

A timeline of over the next 12 to 18 months is probably a reasonable timeline because we have to see that it is not just the price stability but it is also about the economy and the growth which needs to be balanced. Anything which is done prematurely on one dimension has an impact on the other dimensions as well?

Yes 100% India will be. I personally believe that India will be both in top 5 and top 3 with regard to the best performing market. The only thing we have to see is that hopefully it will be on a dollar basis because that is where the currency will come into play and that probably will be a much more robust story and I do believe even there we have a fair chance.

[ad_2]

[ad_1]

Total income of the bank also rose to Rs 21,331.49 crore during July-September period of 2021-22, as against Rs 20,793.92 crore in same period of 2020-21, Canara Bank said in a regulatory filing.

Bank’s gross non-performing assets (NPAs) were a tad up at 8.42 per cent of the gross advances as of September 30, 2021, as against 8.23 per cent by end of September 2020. However, it fell sequentially from 8.50 per cent by end of June 2021 quarter.

In value terms, the gross NPAs stood at Rs 57,853.09 crore, up from Rs 53,437.92 crore.

Net NPAs (bad loans), however, fell to 3.21 per cent (Rs 20,861.99 crore) from 3.42 per cent (Rs 21,063.28 crore).

Provisions for bad loans and contingencies for the reported quarter fell to Rs 3,360.23 crore from Rs 3,974.02 crore in the same period a year ago.

On a consolidated basis, there was a net profit of Rs 1,100.59 crore in September 2021 quarter, up by over two-times from Rs 465.88 crore in year ago period.

Total consolidated income was up at Rs 23,876 crore, from Rs 22,638.26 crore.

Canara Bank stock traded 3.74 per cent down at Rs 194.40 apiece on BSE.

[ad_2]

[ad_1]

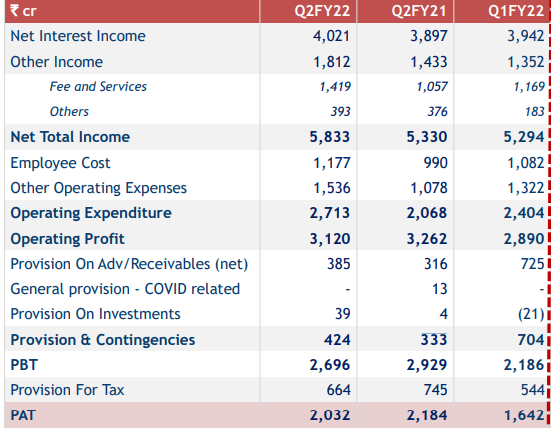

Net interest income (NII) for the bank rose 3 per cent YoY to Rs 4,021 crore from Rs 3,897 crore in the same quarter last year. Net interest margin (NIM) for the quarter came in at 4.45 per cent, the private lender said in a BSE filing.

Gross non-performing assets (GNPA) ratio stood at 3.19 per cent in the September quarter, which was better than 3.56 per cent in the June quarter, but higher than 2.70 per cent (pro-forma) in the year-ago quarter.

Provisions and contingencies for the quarter fell sequentially to Rs 424 crore from Rs 704 crore in the preceding quarter but was higher than Rs 333 crore in the year-ago quarter.

The bank said total provisions, including specific, standard, COVID-19 related ones, stood at Rs 7,637 crore, nearly 100 per cent of gross NPAs. It included Rs 1,279 crore in Covid-19 provisions, which were not utilised during the first half of the financial year.

Provision coverage ratio stood at 67 per cent as on September 30, the bank said in an exchange filing.

Current account deposits grew 32 per cent to Rs 53,280 crore in the September 2021 quarter from Rs 40,454 crore in the year-ago quarter. Savings deposits grew 13 per cent to Rs 1,23,479 crore from Rs 1,08,990 crore YoY.

In accordance with the resolution framework for Covid-19 related stress of individuals and small businesses, announced by RBI, the bank implemented a total restructuring of Rs 495 crore (0.21 per cent of Advances) as at September 30.

Similarly, the bank implemented total MSMEs restructuring of Rs 767 crore (0.33 per cent of advances) as at September 30, the bank said.

[ad_2]

[ad_1]

Investment

oi-Sneha Kulkarni

On Tuesday, Kotak Mahindra Bank reported a 7% year-on-year (YoY) drop in standalone net profit of Rs 2,032 crore, compared to Rs 2,184 crore in the previous quarter. On a quarterly basis, it increased by 24% from Rs 1,642 crore in the June 2021 quarter. Following the earnings report, Kotak Bank’s stock jumped about 3% to 2217 per share on the BSE in Tuesday’s trading.

The bank’s net interest income (NII), which is the difference between interest received and interest expended, increased by nearly 3% to 4,020.6 crore from 3,897 crore the previous quarter. Provisions and contingencies at the private lender fell to 424 crore from 703.5 crore quarter-on-quarter (QoQ), but increased from 333 crore year-on-year (YoY).

In the September quarter, the gross non-performing assets (GNPA) ratio was 3.19 percent, which was lower than the June quarter’s 3.56 percent but higher than the year-ago quarter’s 2.70 percent.

Tax expenses for the quarter ended September fell to 664 crore from 744 crore the previous fiscal quarter. In contrast, its capital adequacy ratio (Basel III) was 21.76 percent, down from 23.11 percent QoQ and 22.05 percent year over year.

COVID-19’s future direct and indirect impact on the Bank’s results of operations, financial condition, and cash flows is unknown and will be determined by current and future events, including attempts to restrict or reduce its spread, it said. As of September 30, 2021, the bank had made provisions of Rs. 1,279 crore for the COVID-19 pandemic.

Over the last three years, net profit per employee has been steadily increasing, with a 13.34 percent increase last year. The stock returned 85.96 percent over three years, compared to 76.81 percent for the Nifty 100. Over a three-year period, the stock returned 85.96 percent, while the Nifty Bank provided investors a 61.47 percent return.

| Parameter | Values |

|---|---|

| Market Cap (Rs. in Cr.) | 436536.94 |

| Earning Per Share (EPS TTM) (Rs.) | 37.13 |

| Price To Earnings (P/E) Ratio | 59.29 |

| Book Value Per Share (Rs.) | 299.66 |

| Price/Book (MRQ) | 7.35 |

| Price/Earning (TTM) | 59.29 |

| ROCE (%) | 12.26 |

| PAT Margin | 25.95 |

| Dividend Yield | 0.04 |

| Face Value | 5 |

[ad_2]

[ad_1]

Planning

oi-Roshni Agarwal

The EPF and pension administering body EPFO via a tweet alerted its members on various scams and asked its members to not deposit money via any of the social channel. Also, it asked subscribers to not respond to similar calls and messages.

#EPFO never asks its members to share their personal details like Aadhaar, PAN, UAN, Bank Account or OTP over phone or on social media.#SocialSecurity #ईपीएफ@byadavbjp @Rameswar_Teli @PMOIndia @PIB_India @PIBHindi @MIB_India @DDNewslive @airnewsalerts @mygovindia @PTI_News pic.twitter.com/kG6UQ5O3mb

— EPFO (@socialepfo) October 23, 2021

IIn a tweet, EPFO said the organisation never asks its members to share their personal details likeAadhaar, P, UAN, Bank Account or OTP over phone or on social media.

And for any type of grievance redressal, the organisation’s members can take up the issue at https://epfigms.gov.in. Additionally members can connect over toll free number 1800-118-005. Also EPF related services can be availed on the government routed platform – UMANG app.

The application offers all such services such as passbook balance, raise as well as track claims, activate UAN as well as other certficates.Pensioners can also get various services related to the passbook, Jeevan Pramaan submission and can also download pension payment orders as well.

GoodReturns.in

Story first published: Tuesday, October 26, 2021, 14:24 [IST]

[ad_2]

[ad_1]

The ₹1,200 crore initial public offer of Fino Payments Bank will open on October 29 and close on November 2. “The price band for the offer has been determined at ₹560 to ₹577 per equity share,” it said on Tuesday.

The IPO size at the upper band is about ₹1,200 crore, comprising ₹900 crore through the offer for sale of 1.56 crore shares and ₹300 crore from fresh issuance of equity shares.

“The company intends to utilise the net proceeds from the fresh issue towards augmenting the bank’s tier-1 capital base to meet its future capital requirements,” it further said.

Also read: Fino Payments Bank gets SEBI nod to float IPO

The company and the selling shareholder have, in consultation with the book running lead manager to the offer, considered participation by Anchor Investors who participation will be on October 28. Axis Capital, CLSA India, ICICI Securities, and Nomura Financial Advisory and Securities (India) are the book running lead manager to the offer.

Fino Payments Bank is a wholly owned subsidiary of Fino Paytech Limited, which is backed by marquee investors like Blackstone, ICICI Group, Intel Capital Corporation, Bharat Petroleum, HAV3 Holdings (Mauritius) and World Bank Arm International Finance Corporation (IFC), among others.

The bank had received market regulator Sebi’s go-ahead for an initial public offering earlier this month. The fintech bank turned profitable in the fourth quarter of 2019-20 and has consistently made profits for seven consecutive quarters.

[ad_2]

[ad_1]

Blockchain-based fan engagement platform SportZchain has raised $4,00,000 in a pre-seed funding round led by Darq Capital. Jagadeesh Atukuri, Director of Comply Dot, and SHISAN Investments (co-founded by EX-COO of Goldman Sachs) among others also participated in the round.

The funds will be utilised to build the platform’s alpha version of an interactive blockchain-based web app and implementing branding & marketing initiatives to drive awareness around its unique offerings.

Also read: Bollywood stars, Indian celebrities launch NFTs amid global craze

Ideated in March 2021, the Singapore-based SportZchain was founded by Siddharth Jaiswal with the belief that sports fans deserve a basic right to be heard by their favourite sports teams, help them make the right decisions by voting on official binding polls, and reap financial gains by owning branded sports token.

The company is backed by Ajeet Khurana (Ex-CEO of Zebpay and Head of Blockchain & Crypto Committee, India), Suhail Chandok (Star Sports TV Presenter, Analyst & Commentator – IPL, ICC Cricket, World Cups, Pro Kabaddi, Wimbledon, etc.), Oksana Belousova (CEO of Fenix Technology), to name a few.

[ad_2]

[ad_1]

ICICI Lombard General Insurance on Tuesday launched the BeFit solution, which will offer customers coverage for their complete OPD requirements, on a cashless basis. “Customers can avail an array of coverage across physical and virtual consultation by general, specialist and super-specialist doctors as well as physiotherapy sessions,” it said in a statement.

Also read: ICICI Lombard Q2 net rises 7.4%

Catering to the other out-of-pocket expenses, the BeFit offering covers pharmacy and diagnostics services related expenses as also those related to minor procedures that do not need hospitalisation. ICICI Lombard’s BeFit benefit along with the standard health insurance policy will provide the policyholder with 360-degree support that they require, it further said.

“This comprehensive offering provides a digitally enabled health ecosystem which is integrated to bring more than 11,000+ doctors across cities. The pharmacy service provides with it express service, that is medicine delivered at home within 60 minutes and lab tests both at home and centre visit. The product also offers 24×7 consultations (tele and virtual) by our panel of expert panel of doctors,” said Sanjeev Mantri, Executive Director, ICICI Lombard General Insurance.

[ad_2]

[ad_1]

Mortgage lender HDFC Ltd and India Post Payments Bank (IPPB) have entered into a strategic alliance to offer home loans to nearly 4.7 crore customers of IPPB.

“Leveraging its extensive and robust country-wide network of 650 branches and over 1,36,000 banking access points (post offices), IPPB aims to make HDFC Ltd’s home loan products and its expertise available to its customers across India,” the two said in a statement on Tuesday.

The partnership aims to facilitate HDFC Ltd’s home loans to customers, especially in unbanked and underserved areas. IPPB will offer housing loans through nearly 1,90,000 banking service providers including postmen and Gramin Dak Sevaks.

J Venkatramu, Managing Director and CEO, IPPB said, “Complemented by our robust network and HDFC’s leadership in the housing finance market, the alliance aims to make housing loans available and accessible, using a digitally-enabled agent banking channel and position IPPB as a one-stop platform for all banking needs of customers, including credit.”

As per the MoU, credit, technical and legal appraisals, processing, and disbursement for all home loans will be handled by HDFC Ltd, while IPPB will be responsible for sourcing of loans.

Renu Sud Karnad, Managing Director, HDFC Ltd said, “IPPB has a strong presence across the country. This strategic alliance will go a long way to promote affordable housing in the remotest locations of our country.”

She further noted that housing is much more affordable today. “In the last couple of years, property prices have more or less remained the same in major pockets across the country while income levels have gone up. Record low-interest rates, subsidies under Pradhan Mantri Awas Yojana and the tax benefits have also helped,” she said.

[ad_2]